Article

How to Prevent Fraud on P2P Marketplaces

Uros Pavlovic

March 5, 2025

Peer-to-peer (P2P) marketplaces have transformed the way people buy, sell, and exchange goods and services. Platforms like Airbnb, eBay, Upwork, and Facebook Marketplace offer users direct transactions without traditional intermediaries. While this model brings convenience, it also introduces significant fraud risks that impact both buyers and sellers.

Scammers have learned to exploit the trust-based nature of P2P platforms, creating fake listings, hijacking legitimate accounts, or fabricating positive reviews to mislead users. In some cases, fraudsters create seemingly legitimate accounts, using disposable emails and phone numbers to operate undetected.

For marketplaces, fraud is more than just a financial risk—it erodes credibility, affects user retention, and attracts regulatory scrutiny.

Why are P2P marketplaces a target for fraud?

Unlike traditional e-commerce platforms that manage transactions directly, P2P marketplaces rely on users to engage with one another. This lack of a centralized authority creates security gaps that fraudsters exploit. The high volume of listings and transactions also makes fraudulent activity harder to detect, allowing scammers to blend in.

Lack of centralized oversight

Many P2P platforms operate with minimal direct intervention, focusing on user-generated content and peer reviews instead of rigorous verification checks. Without strict fraud detection measures in place, fraudsters take advantage of anonymity to manipulate transactions.

High transaction volumes and user turnover

Millions of new listings and sign-ups appear daily across marketplaces, making it difficult to flag fraudulent activity before damage occurs. Marketplaces designed for high turnover, like rental or second-hand sales platforms, face additional risks because users frequently create new accounts, making fraud harder to track over time.

Diverse fraud tactics across different marketplaces

Fraudsters adapt their methods depending on the type of marketplace:

- E-commerce platforms such as eBay or Facebook Marketplace see fake listings, item-not-received scams, and seller fraud.

- Service marketplaces like Upwork or TaskRabbit face identity fraud, fake reviews, and escrow scams.

- Travel marketplaces similar to Airbnb or BlaBlaCar encounter reservation fraud and fake property listings.

The variety of fraud tactics means marketplaces need a dynamic and proactive approach to fraud prevention.

P2P fraud stories and statistics

It doesn't come as a shock that digital fraud is seeing a rise with each passing year. Let's take a look at some of the glowing examples of fraud within the P2P market.

Secondhand clothing apps like Depop and Vinted have seen a rise in scams and hostile interactions. Surveys indicate that 32% of buyers and nearly a quarter of sellers have fallen victim to scams on these platforms. The anonymity and informal nature of these apps have contributed to aggressive bargaining and fraudulent activities (TheGuardian).

In March 2025, cybercriminals exploited a vulnerability in StubHub's system to illicitly obtain nearly 1,000 tickets, primarily for Taylor Swift's Eras Tour, resulting in over $600,000 in profits. This breach underscores the vulnerabilities present in P2P ticket resale platforms and the significant financial incentives for fraudsters targeting high-demand events. (Wired).

In December 2024, Stanley Yee, a 27-year-old photographer from Rosebery, Australia, fell victim to a scam on Facebook Marketplace. Although police facilitated a refund after tracking the seller through Facebook and PayPal details, no charges were pressed as there was no financial loss, and Yee had put himself in the car. (News.com.au).

These multiple cases show just how much P2P platforms are at risk. Overall, judging from the fraud statistics we've witnessed in the past year, these risks do not show any signs of waning. If anything they appear to be growing.

Common types of P2P marketplace fraud

Fraud in P2P marketplaces takes many forms, often targeting both buyers and sellers. While some schemes focus on deceiving individual users, others exploit weaknesses in platform security to operate at scale. Understanding the most prevalent fraud types helps marketplaces identify vulnerabilities and implement stronger safeguards.

Fake listings and payment fraud

Fraudsters frequently create non-existent product or service listings to lure buyers into making payments for items that don’t exist. Scams involving electronics, vehicles, and rental properties are among the most common, with fraudsters disappearing as soon as a payment is made. A more sophisticated version of this scheme involves fake escrow services. Buyers are directed to what appears to be a secure third-party payment system, only to realize later that the website was fraudulent. Since transactions often happen outside the platform, recovering lost funds becomes nearly impossible.

Account takeover (ATO) and synthetic identity fraud

Compromised accounts pose one of the biggest threats to P2P marketplaces. Fraudsters use stolen credentials to gain access to legitimate user accounts, allowing them to pose as trusted buyers or sellers. Once inside, they modify payment details, engage in scams under the user’s name, or withdraw funds. Marketplace platforms that rely solely on password-based authentication are particularly vulnerable, as fraudsters often acquire login credentials through data breaches or phishing attacks. In some cases, synthetic identities—combinations of real and fabricated user data—are created to bypass weak identity verification systems.

Fake reviews and seller manipulation

Reputation plays a critical role in P2P marketplaces, which is why fraudsters use fake reviews to manipulate buyer decisions. A network of fraudulent accounts can artificially boost the credibility of a scammer’s profile, making their listings seem more trustworthy. Alternatively, fraudulent actors target legitimate sellers, bombarding them with negative reviews in an attempt to damage their reputation or force them off the platform. This manipulation distorts the marketplace’s rating system, making it harder for users to distinguish between genuine and fraudulent sellers.

Fraudulent chargebacks and refund abuse

Certain P2P fraud schemes rely on exploiting chargeback policies. Buyers may falsely claim that they never received an item, forcing the marketplace to issue a refund while they keep the product. Some fraudsters escalate this strategy by using stolen payment methods, where the real account owner eventually disputes the transaction, leading to losses for sellers and platforms. Refund fraud can be difficult to detect, especially when marketplaces lack risk scoring mechanisms to identify suspicious behavior patterns. Without advanced verification methods, platforms remain vulnerable to repeated chargeback fraud attempts.

Unauthorized access and multi-account fraud

Many fraudsters operate multiple fake accounts to maximize their reach on a marketplace. Some create seller profiles to list fake products, while others pose as buyers to validate fraudulent listings or commit payment fraud. This type of fraud often involves the creation of synthetic identities, IP manipulation, device spoofing, and disposable email accounts. Without proper detection systems in place, fraudsters can continue creating new accounts even after previous ones are flagged or suspended.

What’s at stake? The real cost of P2P fraud

P2P marketplaces thrive on trust. Without a secure and reliable environment, users hesitate to engage, transactions decline, and platforms struggle to retain their customer base. Fraud not only creates immediate financial losses but also damages long-term credibility, affecting growth and sustainability.

Loss of trust and reputation damage

Trust is the foundation of any P2P platform. When buyers encounter scams or sellers experience chargeback fraud, confidence in the marketplace erodes. Negative experiences spread quickly through social media and online reviews, making it difficult to attract new users and retain existing ones. Once a marketplace gains a reputation for fraud-related issues, regaining trust becomes an uphill battle. Users are more likely to seek alternative platforms, reducing transaction volumes and long-term profitability.

Financial losses from fraud-related incidents

Every fraudulent transaction carries a cost. Whether it’s reimbursing victims, absorbing chargeback fees, or investing in additional fraud prevention measures, the financial impact adds up quickly. Some fraud cases involve large-scale operations where criminals exploit loopholes to steal money from multiple accounts. Without proactive fraud detection mechanisms, platforms remain vulnerable to repeat offenders who refine their tactics over time.

Compliance risks and regulatory challenges

Regulatory bodies increasingly expect online marketplaces to implement robust fraud prevention measures, especially when handling financial transactions. Platforms that fail to prevent fraud may face regulatory scrutiny, fines, or even legal action. For marketplaces operating in multiple regions, compliance with data protection laws, KYC (Know Your Customer) regulations, and anti-money laundering (AML) requirements becomes essential. A lack of proper fraud detection and identity verification solutions can expose platforms to regulatory penalties.

Increased user churn and abandonment

Fraud doesn’t just affect direct victims—it impacts the entire ecosystem. When users feel unsafe, they hesitate to engage in new transactions or abandon the platform entirely. Higher churn rates mean lower revenue and reduced platform engagement, forcing businesses to spend more on customer acquisition just to maintain the same level of activity. A secure environment encourages repeat transactions and long-term engagement, making fraud prevention a key component of marketplace sustainability.

How to prevent P2P fraud with Identity Intelligence

Fraud prevention in P2P marketplaces requires more than just traditional identity verification. Fraudsters are skilled at bypassing KYC (Know Your Customer) checks using stolen identities, synthetic profiles, and disposable contact details. A more effective approach involves analyzing digital signals, uncovering hidden connections between fraudulent accounts, and detecting risk indicators in real time.

Strengthening account opening protection

Fraud often begins at the moment of sign-up. If bad actors gain access to a platform, they can operate freely, setting up fake listings or purchasing items they plan to dispute. Identifying fraudulent sign-ups before they cause damage is critical to keeping the platform secure. Businesses can assess whether a new user exhibits high-risk characteristics by analyzing email, phone, and IP data during registration. Certain signals—such as the use of temporary email addresses, newly registered phone numbers, or mismatched geolocation data—can indicate fraud before any transactions take place.

Using OSINT and digital signal analysis to verify users

Open-Source Intelligence (OSINT) provides additional insights into whether a user is who they claim to be. Fraudsters often rely on anonymous digital footprints, but background analysis of their email history, phone registration, and online activity can reveal inconsistencies.

- Email Address Analytics: does the email belong to a recently created domain? Is it linked to past data breaches?

- Phone Number Intelligence: has the phone number been associated with multiple accounts? Is it a virtual or disposable number?

- IP Address Intelligence: is the IP linked to a VPN, proxy, or a high-risk location?

These checks run in the background without introducing friction, helping platforms detect suspicious users before they interact with legitimate buyers and sellers.

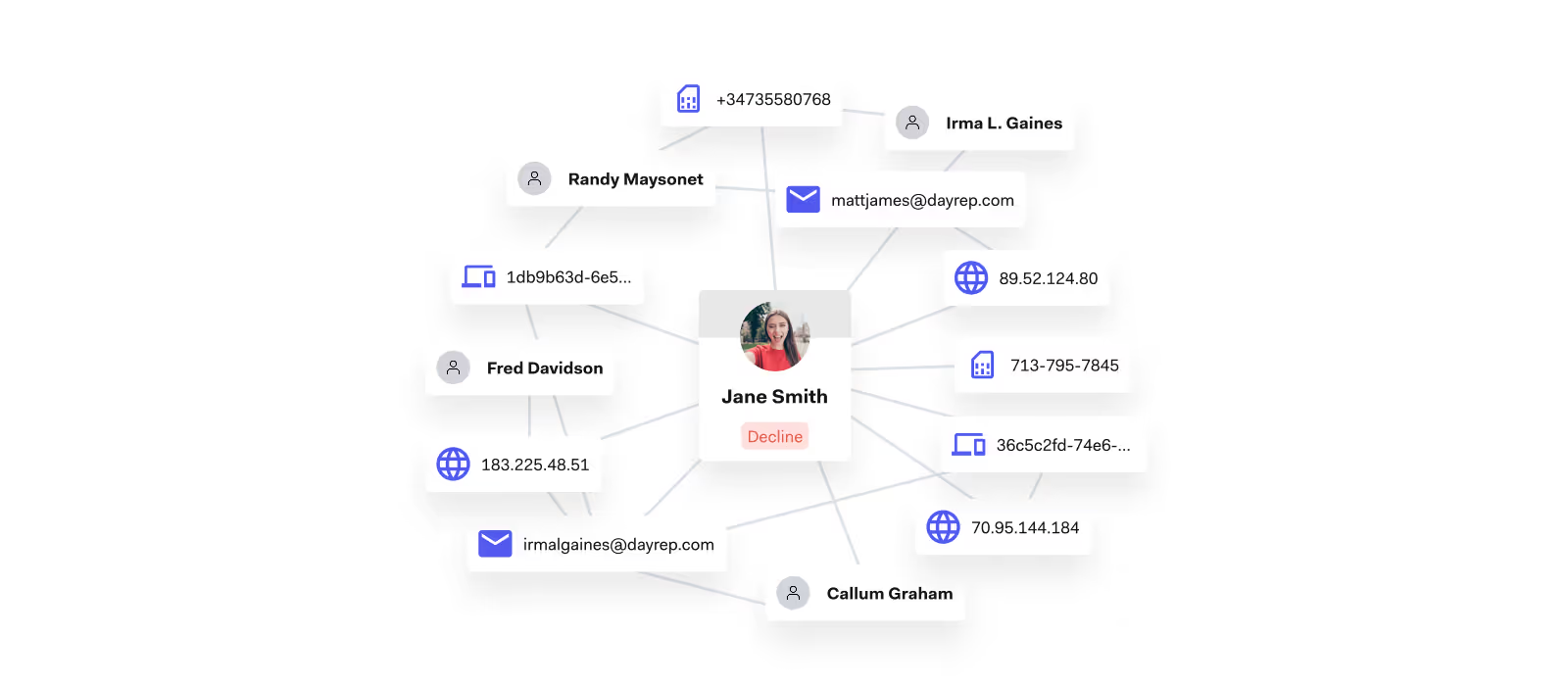

Detecting unusual patterns and suspicious links between accounts

Many fraudsters operate multiple fake accounts to build credibility or conduct large-scale scams. Identifying connections between users—such as shared devices, login locations, or email domains—helps flag fraudulent activity before it escalates. Advanced fraud prevention tools use graph-based analysis to map relationships between seemingly unrelated accounts. For example, if multiple users share the same IP address, browser fingerprint, or device ID, there’s a high likelihood of coordinated fraud.

Preventing unauthorized access and account takeover

Even if an account starts out legitimate, fraudsters often attempt account takeovers (ATO) by using stolen credentials. Once inside, they may change payment details, withdraw funds, or run scams under a trusted profile. Preventing ATO requires more than just passwords. Real-time Login Authentication protects existing user accounts by analyzing:

- Unusual login behavior (e.g., unusual or bot-like keystroke dynamics and mouse movements).

- Device inconsistencies (e.g., accessing the platform from an unfamiliar device).

- High-risk IPs (e.g., logins from known fraud hotspots or anonymized networks).

Ongoing risk assessment of user activity helps detect fraudsters early, preventing them from causing harm.

Why traditional IDV isn’t enough

Many P2P marketplaces try to prevent fraud by requiring users to submit government-issued IDs, credit card verifications, or facial recognition scans during onboarding. While these measures add a layer of security, they are not foolproof.

For instance, identity documents are frequently stolen, forged, or purchased on the dark web. Fraudsters use these documents alongside a combination of real and fabricated credentials to bypass ID verification checks and standard KYC measures.

Real-time detection of suspicious contact details

Fraudsters often use phone numbers and email addresses that appear valid during onboarding, but certain clues can reveal they were created for fraudulent purposes.

A deeper risk assessment of phone and email data can reveal:

- Email domains with no prior digital footprint, signaling a newly created email.

- Disposable or virtual phone numbers, used to bypass verification steps.

- Phone numbers linked to multiple accounts, indicating possible fraud rings.

Forcing users to go through multiple identity verification steps can introduce friction, discouraging legitimate sign-ups. While fraudsters find ways to work around ID verification, honest users may abandon the platform if onboarding takes too long or requires too many steps.

A more effective fraud prevention approach involves silent checks that don’t disrupt user experience. Online businesses can assess risk in the background by examining digital signals on users' phone numbers, email addresses, but also IP and device data, ensuring a seamless user experience.

Instead of relying solely on ID verification, marketplaces should adopt a multi-layered fraud detection system that incorporates:

- Pre-screening of email, phone, and IP data at sign-up.

- Risk-based scoring models that detect high-risk behavior patterns.

- Graph-based analysis to uncover fraudulent account networks.

- Login Authentication to prevent account takeovers (ATO). Advanced authentication methods detect unauthorized access attempts by assessing device consistency, IP risk, and unusual login behavior in real-time.

Fraud prevention should not be a one-time check during onboarding—continuous monitoring of user activity ensures that fraudsters are detected before they can cause harm.

For a more comprehensive insight into P2P marketplace fraud, please contact our team of experts to determine exactly the right strategy for your organization.