Article

Preventing Fraud in Instant Payments: Insights on New EU Parliament Legislation and PSP Responsibilities

Uros Pavlovic

February 23, 2024

In an age when financial transactions match the pace of our digital lives, the European Parliament has taken a significant step forward. On February 7, 2024, new rules were adopted that promise to transform the landscape of financial transfers within the European Union. This legislation mandates that funds transferred across the EU must now arrive in the recipient's bank account within a mere ten seconds, a change that marks a significant leap towards modernizing payments in the European single market.

Transforming the European payment landscape

At the heart of this legislative shift is the instant credit transfer, a mechanism designed to operate 24/7, ensuring that money is transferred almost instantaneously. This innovative approach to financial transactions is set to benefit not just individual consumers but also businesses, and small and medium-sized enterprises (SMEs) that often rely on the swift movement of funds. The European Parliament's decision underscores a commitment to not only speed but also the safety and reliability of these transactions. By ensuring that funds are made available within ten seconds, the new regulation addresses a longstanding inconvenience: the days-long wait that customers and businesses previously endured.

The instant payment system is poised to redefine the standards of financial transactions across the EU. It transcends the traditional banking hours, offering flexibility and efficiency that align with the dynamic nature of today's economy. The inclusivity of this system is further evidenced by its applicability to member states outside the eurozone, albeit with a provision for a longer transition period. This flexibility ensures that the benefits of instant payments can be widely enjoyed, fostering a more interconnected and efficient European market.

Enhancing consumer safety and trust

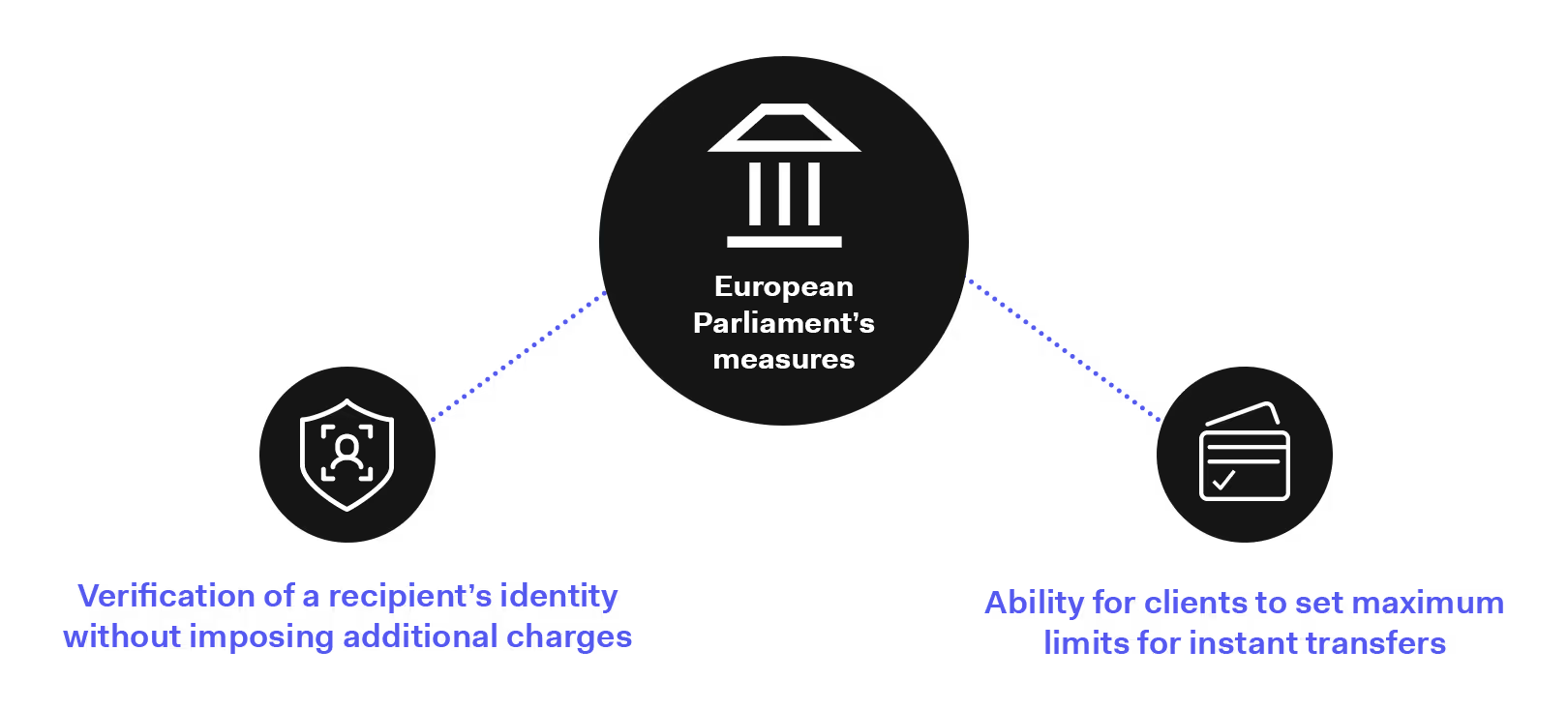

With the advent of instant payments comes an increased focus on the security of these transactions. The European Parliament has placed consumer safety at the forefront of its agenda, mandating that banks and other Payment Service Providers (PSPs) implement robust and up-to-date fraud detection systems. These measures are crucial in an environment where the speed of transactions could potentially be exploited by fraudulent actors. By requiring the verification of a recipient's identity without imposing additional charges, the new rules aim to build a safer financial ecosystem for all EU citizens.

This emphasis on safety is not just about protecting funds; it's about fostering trust in the European financial system. The ability for clients to set maximum limits for their instant transfers adds another layer of security, giving individuals and businesses more control over their finances. These provisions demonstrate a holistic approach to financial security, combining speed, efficiency, and safety in a way that significantly benefits consumers and the economy at large.

New rules for Payment Service Providers (PSPs)

In the wake of these groundbreaking changes, Payment Service Providers (PSPs) find themselves at the forefront of a significant operational overhaul. Under the new regulations, PSPs are mandated to ensure that credit transfers are not only affordable but also processed with unprecedented immediacy. This requirement heralds a new era of financial transactions, where efficiency and cost-effectiveness are paramount.

More critically, PSPs are now tasked with implementing state-of-the-art fraud detection and prevention systems. This move is indicative of a broader shift towards enhancing digital trust and security in the financial sector. PSPs must offer services that allow for the immediate verification of a recipient's identity at no extra cost to the consumer. This approach is not merely about safeguarding transactions; it's essential to building a more secure and resilient financial ecosystem.

Furthermore, the legislation empowers clients by allowing them to set a cap on the maximum amount for instant credit transfers. This provision adds a layer of personal security, enabling users to tailor their transaction limits according to their individual needs or concerns.

Regulatory framework and penalties

The European Parliament's legislation does not shy away from establishing strict guidelines and consequences for PSPs that fail to align with their fraud prevention duties. A significant aspect of this regulatory framework is the introduction of a liability shift. Should a PSP neglect its obligations in conducting thorough analyses of recipients and implementing robust fraud prevention measures, it could be held liable for any resultant financial damages suffered by the client.

This liability shift represents a crucial change in the financial landscape, placing a greater emphasis on the responsibility of PSPs to protect their clients from fraud. It underscores the necessity for PSPs to adopt comprehensive and effective strategies in fraud detection and prevention.

In addition to the liability shift, the framework also mandates PSPs to conduct checks ensuring that none of their clients are subject to sanctions or other restrictive measures associated with money laundering and terrorist financing. This requirement highlights the importance of vigilance and due diligence in the fight against financial crimes, further enhancing the integrity of the European financial system.

The penalties for non-compliance are clear and significant. PSPs that fail to meet these new standards risk not only financial repercussions but also the potential erosion of consumer trust, which is indispensable in the digital age. These regulations set a new benchmark for the level of security and reliability expected of financial institutions, pushing the industry toward a more secure and transparent future.

Impact on charges for instant credit transfers

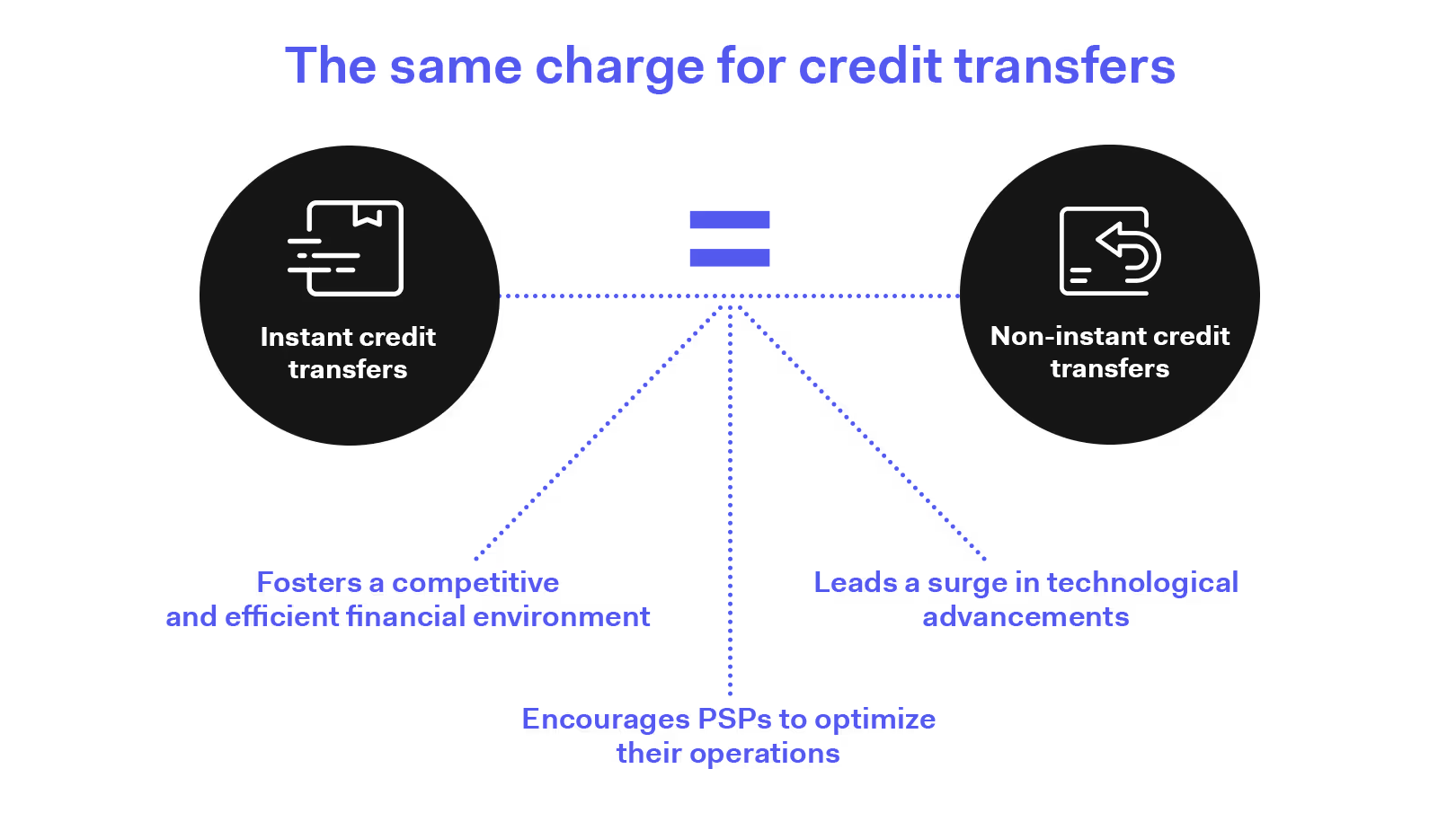

A pivotal aspect of the European Parliament's legislation is its approach to the cost associated with instant credit transfers. In a move that aligns with the broader objectives of accessibility and fairness, the regulation stipulates that charges for instant transactions cannot exceed those applied to traditional "non-instant" credit transfers. This decision is instrumental in democratizing access to instant payments, ensuring that the benefits of rapid transactions are not overshadowed by prohibitive costs.

The significance of this rule cannot be overstated. It addresses one of the primary concerns among consumers and businesses alike: the fear of increased transaction costs. By capping the fees for instant transfers at the level of conventional transactions, the legislation not only promotes the adoption of instant payments but also safeguards the interests of users, ensuring that the financial burden does not deter them from leveraging the advantages of this modern payment system.

This approach reflects a commitment to fostering a competitive and efficient financial environment where the focus remains on enhancing the user experience without compromising on cost. It encourages PSPs to optimize their operations and invest in technologies that can handle the demands of instant payments efficiently, thereby minimizing the need for additional charges.

Moreover, this regulation serves as a catalyst for innovation within the financial sector. PSPs are now more incentivized than ever to develop cost-effective solutions to facilitate instant transactions. This, in turn, could lead to a surge in technological advancements aimed at reducing operational costs, enhancing security, and improving transaction speeds, further enriching the financial ecosystem.

In essence, the decision to equalize the charges for instant and non-instant credit transfers is a strategic move designed to accelerate the transition towards a more agile and user-friendly payment system across the European Union. It embodies the spirit of modernization that the legislation seeks to instill in the financial landscape, ensuring that the advantages of instant payments are accessible to all, without financial constraints.

Instant payment modernization and legislative impact

Michiel Hoogeveen, the lead Member of the European Parliament (MEP) for this legislation, encapsulated the transformative nature of the Instant Payments Regulation with his statement: “The Instant Payments Regulation marks the long-awaited modernization of payments in the European single market. Customers can now say goodbye to the inconvenience of waiting two or three working days to access their money. We are delivering on something that people and businesses truly care about transferring money within 10 seconds at any time of the day.”

The overwhelming support for the legislation, evidenced by the vote count of 599 to 7 with 35 abstentions, signifies a broad consensus on the importance of modernizing the EU's payment infrastructure. The next steps involve the publication of the new rules in the EU Official Journal, followed by a phased implementation period. PSPs located in the euro area will have 9 months to prepare for receiving instant credit transfers in euro and 18 months to initiate them, marking a significant milestone in the EU's journey towards financial innovation and inclusion.

The role of technology in compliance and fraud prevention

The centerpiece of this legislative overhaul is the undeniable role of technology in enabling PSPs to meet their new obligations. Advanced solutions, particularly those leveraging machine learning and alternative data (such as phone, email, IP, browser, and device information), are set to become indispensable tools in the arsenal against fraud.

For PSPs, interpreting digital signals through Machine Learning (ML) offers a strong mechanism for real-time fraud detection and prevention. Such platforms can analyze vast amounts of data to identify suspicious patterns, verify the identity of recipients, and ensure transactions comply with the new regulatory mandates. This not only aids in fraud prevention but also enhances the speed and reliability of transactions, aligning with the objectives of the new regulation.

Furthermore, the ability of these technologies to adapt and learn from new fraud tactics over time ensures that PSPs can maintain a high level of security and compliance, even as threats evolve. This dynamic capability underscores the importance of investing in sophisticated, future-proof solutions that can support the instant payments ecosystem's growth and resilience.

Elevating consumer trust with risk intelligence

The European Parliament's new regulation on instant payments represents a significant leap forward for the financial sector, emphasizing speed, security, and accessibility. As PSPs navigate these changes, the integration of advanced technological solutions will be critical to achieving compliance and safeguarding consumer trust. This momentous shift not only enhances the efficiency of financial transactions but also sets a new standard for innovation and consumer protection in the digital age.

To discover some of the latest risk intelligence advancements that can help build up your fraud prevention defenses:

- Rule Builder - create complex rules with a simple interface, with no coding involved, work fast with a powerful autocomplete, browse our rule bank to build your starter pack, and more.

- Insights - by collecting a wide range of data the feature will allow you to easily identify trustworthy customers. At the same time, you can use Insights to red-flag suspicious activity, thus isolating potential fraudsters.

- Graph - a feature designed to establish powerful and reliable connections between various digital identifiers. By weaving a web of associations, Trustfull can now pinpoint unusual patterns and identify potentially suspicious activities related to new signups, transactions, or logins.

For more detailed information, reach out to our team of fraud prevention experts.