Article

What's FRAML's Role in Preventing Financial Fraud?

Uros Pavlovic

February 6, 2024

In today’s fast-paced and primarily digital financial world, fraud and money laundering have become ever-present and increasingly interconnected. The FRAML framework takes a holistic approach to combating both threats. Short for "Fraud and Anti-Money Laundering", FRAML is increasingly seen as a crucial defense against financial crime. But what does it really mean, and why does it matter? This guide breaks down how FRAML works, the tools needed to implement it, and its role in keeping our financial systems secure.

What is FRAML, and why does it matter?

Fraud and money laundering may operate through different mechanisms, but they often intersect, exploiting the same vulnerabilities across financial systems. This growing overlap has exposed the limitations of tackling these issues in isolation. As financial crime becomes more digitally sophisticated, the industry is shifting toward an integrated model: FRAML, short for Fraud and Anti-Money Laundering.

More than just a buzzword, FRAML represents a collaborative approach to fraud and AML, combining insights, technology, and strategy to improve detection and response. While fraud teams usually focus on behavioral patterns and real-time risk signals, AML teams are trained to track illicit money flows and maintain compliance. FRAML doesn't erase those distinctions—it connects them, allowing institutions to better protect themselves without duplicating efforts or overlooking blind spots.

Statistics: scam and fraud impact

The growth in popularity of FRAML is in part driven by the financial industry’s need to find more effective countermeasures to rising fraud and money laundering threats.

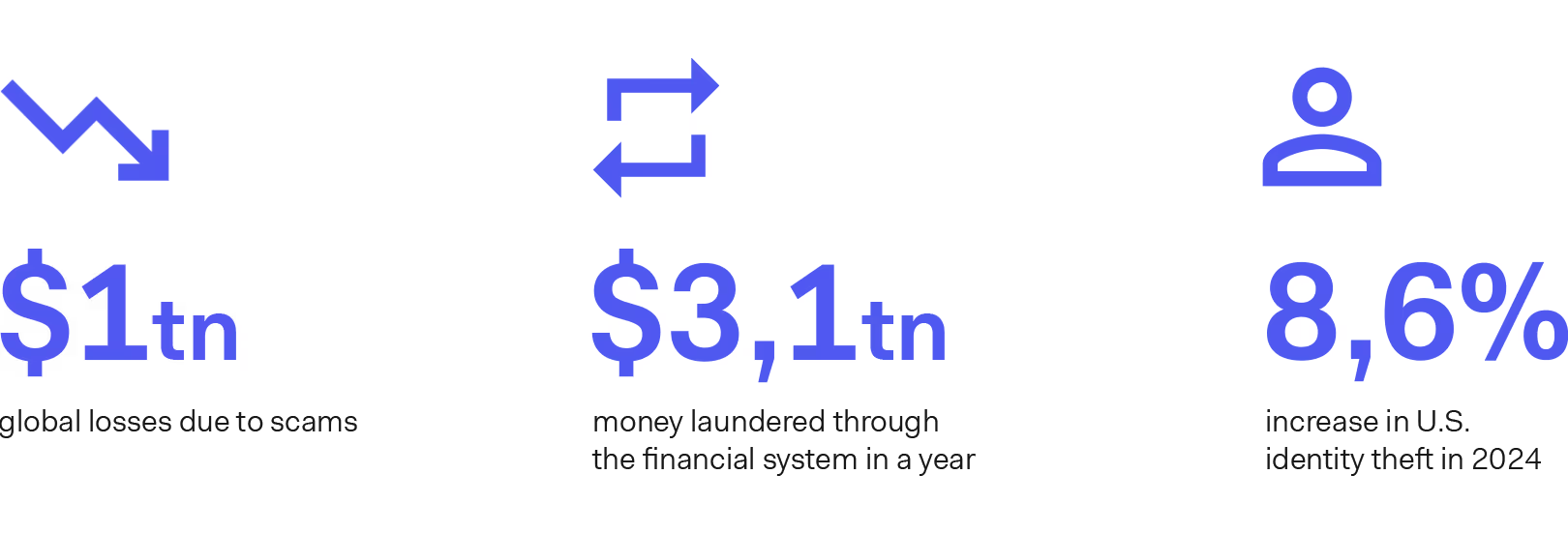

According to the 2024 Global State of Scams report, scams are costing consumers over $1 trillion globally. Additional data from the Federal Trade Commission shows a huge increase in losses due to fraud, which in the U.S. alone amounted to $12.5 billion in 2024 (Source: FTC).

In 2023, an estimated $3.1 trillion in illicit funds moved through the global financial system, funding a wide range of serious crimes, including $346.7 billion in human trafficking, $782.9 billion in drug trafficking and $11.5 billion in terrorist financing. That same year, global losses from fraud—including scams and bank-related schemes—reached $485.6 billion, underscoring the scale and urgency of financial crime worldwide (Source: Nasdaq).

Finally, identity theft is also on the rise: in the US there were 1,135,291 cases of identity theft reported during 2024, which marks an 8.6% increase compared to the previous year. Out of all types of identity theft, credit card fraud was the most common.

As fraud and money laundering cases become increasingly common, industry experts and law enforcement are gaining a clearer understanding of how deeply connected these two crimes are. In fact, those who commit fraud typically need a method to conceal or move their illicit earnings, while money launderers frequently use fraudulent activity as a vehicle for disguising the origin of criminal funds.

But how are financial institutions fighting back against this dual risk of fraud and money laundering? And are traditional AML and anti-fraud methods still effective against modern fraudsters?

The limits of traditional AML and fraud defenses

For years, the financial sector has relied on a mix of mostly disconnected KYC procedures, AML screening, and anti-fraud tools to maintain compliance and detect suspicious activity. While each component plays an important role, the lack of integration across these systems can significantly reduce the overall effectiveness of fraud and anti-money laundering efforts.

In particular, while KYC checks and AML screening are essential compliance measures, they are not designed to detect fraud. Fraudsters today operate in a gray zone, often passing KYC and AML checks with stolen or synthetic identities. A common scenario: someone buys a stolen identity off the dark web, signs up with a disposable phone number and a newly created email, and uses a VPN to spoof their location. The result? They slip past verification and enter the system undetected—until it’s too late.

At the same time, fraud prevention tools aren’t always effective at preventing money muling and money laundering practices down the line. A legitimate user or small business might willingly act as a money mule, letting illicit funds pass through their previously approved - and perfectly legitimate - account in exchange for a commission. Since they’ve already passed fraud and KYC checks, this behavior may not be flagged without behavioral or contextual insight.

This disconnect is precisely why FRAML is gaining traction. It’s not just about merging functions—it's about recognizing that fraud and money laundering are often symptoms of the same root vulnerabilities and require a more connected, data-driven response.

FRAML in practice: a strategic mindset over a team merger

While it might be tempting to think of FRAML as simply merging fraud and AML departments, this interpretation is often too narrow—and, in many cases, operationally unworkable. Fraud and AML teams serve different regulatory obligations, possess distinct expertise, and operate on different timelines.

Instead, FRAML should be viewed as a shared philosophy—a strategic model that promotes alignment without forcing all systems to merge into one. It’s about collaboration over consolidation: sharing relevant data, coordinating risk models, and using unified technologies where appropriate. This approach fosters stronger detection capabilities without sacrificing the specialized focus each function requires.

What makes FRAML challenging to implement?

Despite its promise, implementing FRAML comes with real hurdles that extend beyond organizational charts. One of the most persistent challenges lies in the skill gap between fraud and AML professionals. Fraud teams tend to be geared toward real-time intervention and behavioral analysis, while AML analysts focus on long-term investigations, regulatory filings, and audit trails. These areas require different training, tools, and day-to-day workflows.

On top of that, regulatory requirements diverge significantly. For example, AML teams in many jurisdictions must submit Suspicious Activity Reports (SARs), whereas fraud cases may involve different reporting processes altogether—often through internal systems or law enforcement channels. Then there’s the issue of team structure and expectations.

Financial institutions aiming to cut costs might view FRAML as an opportunity to shrink headcount by collapsing two departments into one. But without clear roles, supporting technology, and structured workflows, this shortcut can lead to compliance risks, operational confusion, and even higher exposure to financial crime.

Key enablers of a successful FRAML strategy

For FRAML to deliver meaningful results, financial institutions need more than just shared intent—they need the right systems, infrastructure, and feedback mechanisms in place. The most successful implementations are built around three core pillars:

- Ongoing feedback loops between fraud and AML teams, where alerts and investigations from one function help refine the risk models of the other.

- Seamless technology integration through APIs and shared platforms, enabling data to flow freely without duplication or lag.

- Cloud-ready infrastructure that allows teams to access up-to-date data in real-time, with safeguards for GDPR and other regulatory requirements.

These elements make it possible to coordinate decision-making across teams, eliminate silos, and strengthen the organization’s response to emerging threats—all without compromising data privacy or regulatory compliance.

Who benefits the most from FRAML?

Any financial organization can apply FRAML principles, but some business models are especially well-suited to embrace this approach from the start. Let’s take a closer look:

- Fintech startups benefit from embedding FRAML into their operations early, especially since they often work with limited historical data. Establishing shared workflows and technology between fraud and AML functions helps ensure scalability and compliance as they grow.

- Banks with in-house analyst teams—regardless of size—often have the necessary visibility and infrastructure to align fraud and AML processes effectively.

- Crypto platforms, already under increasing regulatory scrutiny, face threats that often span both fraud and money laundering. For these firms, a unified FRAML model enables faster detection and reduces the risk of oversight in high-risk environments.

For all of these organizations, FRAML is not a plug-and-play solution—but when implemented thoughtfully, it can offer a major strategic advantage.

The infrastructure behind effective FRAML

Building an effective FRAML framework requires more than aligning goals and teams — it demands the right technology stack to support coordinated workflows and accurate decision-making. The systems that underpin FRAML must be able to connect, scale, and evolve with changing regulatory and risk landscapes.

Three key components often define a robust FRAML infrastructure:

- API-first architecture – to eliminate data silos, fraud and AML systems must communicate fluidly. Well-documented REST APIs allow different tools to exchange data in real time, reducing duplication and keeping risk assessments current across functions.

- Cloud-native platforms – cloud infrastructure provides the agility needed to manage high volumes of data, especially when fraud and AML functions are working off the same sources. It also simplifies compliance with global data privacy standards by offering region-based storage and access controls.

- ML-powered risk models – Machine Learning plays an increasingly important role in identifying fraud and money laundering indicators. When algorithms are trained on datasets spanning both domains, institutions can spot early warning signs that may otherwise go unnoticed in isolated systems.

Ultimately, technology serves as the backbone of the FRAML approach, ensuring that teams can collaborate without sacrificing speed, accuracy, or regulatory control.

The case for FRAML

As financial crime continues to evolve in scale and complexity, separating fraud and AML efforts is no longer practical. Institutions need an approach that reflects the interconnected nature of today’s threats—without compromising on regulatory integrity or operational focus. FRAML provides that middle ground: not a merger of teams, but a model for smarter collaboration, shared intelligence, and cohesive infrastructure.

In a landscape where compliance gaps and data silos can lead to serious risk exposure, FRAML isn’t just a strategy—it’s becoming a necessity.

Discover how to shield your business from fraud and improve digital fraud detection methods.