Article

Merging Simplified Due Diligence with Identity Intelligence Precision

Uros Pavlovic

September 25, 2024

Effective compliance practices are essential for financial institutions to manage risk and meet regulatory demands. Simplified Due Diligence (SDD) is a key aspect of the risk-based strategies enforced by international financial regulators. SDD allows businesses to efficiently verify customers who have been identified as “low-risk”, especially during the onboarding phase. However, ensuring that only those qualifying for SDD are routed through this expedited process is crucial to avoid potential regulatory pitfalls. In this article, we explore the regulatory anti-money laundering principles and traditional methods of performing SDD, before delving into how identity intelligence based on users’ email, phone, and IP address can bolster the process and protect businesses against risky oversights.

What is SDD (Simplified Due Diligence)?

Simplified Due Diligence is a compliance measure designed for customers who are identified as low-risk, allowing financial institutions to expedite their identity verification process. Customers who present minimal risk can be fast-tracked through an SDD process, helping businesses reduce onboarding times, contain compliance costs, enhance the customer experience and focus time and resources on applicants and customers presenting a higher risk. However, as with any compliance measure, SDD must be carefully applied within a regulatory framework and based on a thorough understanding of which customers qualify for this streamlined approach.

Let’s dig deeper into the fundamentals of Simplified Due Diligence, the regulatory frameworks that support its use, traditional methods for determining customer eligibility, and how cutting-edge solutions—specifically identity intelligence and digital signals—can secure the process of SDD. The goal is to help professionals in financial services, banks, and fintechs better understand how to meet SDD compliance requirements while also enriching their customer data with valuable trust and risk signals.

The risk-based approach to compliance and SDD

The concept of Simplified Due Diligence is deeply rooted in the risk-based approach to compliance, a cornerstone of modern regulatory frameworks in financial services. Rather than adopting a one-size-fits-all strategy, this approach requires financial institutions to tailor the level of due diligence to the potential risks posed by individual customers. The rationale is simple: not all customers present the same level of risk when it comes to activities such as money laundering, fraud, or terrorist financing.

In a risk-based model, customers are classified according to their risk profile—ranging from low to high risk. High-risk customers, such as politically exposed persons (PEPs) or those with complex financial transactions, require Enhanced Due Diligence (EDD), which involves a more rigorous investigation of their background, source of funds, and financial history. On the other end of the spectrum, low-risk customers—those deemed unlikely to engage in illegal activities—qualify for Simplified Due Diligence.

SDD is essentially a fast-tracked due diligence process applied to these customers. Instead of conducting an exhaustive investigation, financial institutions perform fewer checks and rely on basic verification methods. This minimizes the administrative burden and shortens onboarding times, making SDD particularly useful for sectors with a high volume of customers, such as retail banking, payment services, or low-risk investment products.

The criteria for identifying low-risk customers typically include factors such as:

- Customer profile consistency: low-risk customers often exhibit consistent information across multiple data points provided during onboarding, such as name, address, and contact details. Customers with no discrepancies between these data points—such as mismatched addresses or phone numbers—are typically considered less risky.

- Geographic location: customers from regions with strong AML regulations, such as the EU or FATF-compliant countries, are often deemed lower risk. Location data provided during onboarding, such as country of residence or business registration, plays a significant role in assessing the customer's risk level.

- Customer type: known customers, regulated entities, and public companies are often considered low-risk. Institutions may rely on data from previous customer relationships or public information (e.g., stock exchange listings) to determine that these customers pose minimal financial crime risk.

The risk-based approach not only helps financial institutions allocate resources more effectively but also facilitates ongoing compliance with local and international regulations.

In this context, Simplified Due Diligence provides businesses with a way to verify customers without compromising the speed and ease of onboarding, ensuring that compliance doesn’t come at the cost of customer satisfaction. However, the application of SDD must be backed by a thorough understanding of regulatory requirements, which differ across jurisdictions.

Regulatory framework for Simplified Due Diligence

The application of Simplified Due Diligence (SDD) is not universal; it is guided by regulatory frameworks that vary across countries and regions. These frameworks outline when and how financial institutions can implement SDD, focusing on identifying low-risk customers and transactions that do not require the same level of scrutiny as higher-risk individuals or entities.

One of the most significant regulatory bodies influencing SDD practices is the Financial Action Task Force (FATF), an intergovernmental organization that sets international standards for combating money laundering, terrorist financing, and other financial crimes. FATF’s recommendations form the foundation of many countries’ AML laws and regulations, and they explicitly allow for a risk-based approach to Customer Due Diligence (CDD). According to the FATF, financial institutions are permitted to apply Simplified Due Diligence measures to customers who are identified as low-risk.

In the European Union, the series of Anti-Money Laundering Directives provide a clear framework for the use of SDD. AMLD4, which came into effect in 2017, and the subsequent versions of the EU Directive require financial institutions to perform due diligence on their customers but also acknowledge that not all customers present the same level of risk. The directives set out specific criteria for identifying low-risk customers, such as the nature of the business relationship and the geographical area involved.

In the United Kingdom, SDD is allowed under the Money Laundering, Terrorist Financing and Transfer of Funds Regulations 2017, which closely align with the aforementioned FATF guidelines and AMLD4. UK regulators also stipulate that SDD should not be applied in cases where the business has any reason to suspect that the customer is involved in criminal activity.

Beyond the EU and the UK, many other jurisdictions have adopted similar provisions based on FATF’s guidelines. For example:

- Australia’s Anti-Money Laundering and Counter-Terrorism Financing Act 2006 permits SDD for customers with low-risk profiles.

- Canada’s Proceeds of Crime (Money Laundering) and Terrorist Financing Act (PCMLTFA) allows financial institutions to use SDD for certain customer types, such as government entities or publicly listed companies.

- In the United States, while SDD is not explicitly outlined in the Bank Secrecy Act (BSA), a risk-based approach to AML compliance is encouraged, allowing for reduced due diligence in cases of low-risk customers.

These frameworks enable businesses to streamline their onboarding and compliance processes for low-risk customers while maintaining the necessary checks to prevent money laundering and fraud. However, financial institutions must ensure they fully understand the legal boundaries within their operating regions and apply SDD appropriately. Misuse of SDD, such as applying it to customers or transactions that do not meet the low-risk criteria, can result in regulatory penalties and reputational damage.

The process of Simplified Due Diligence

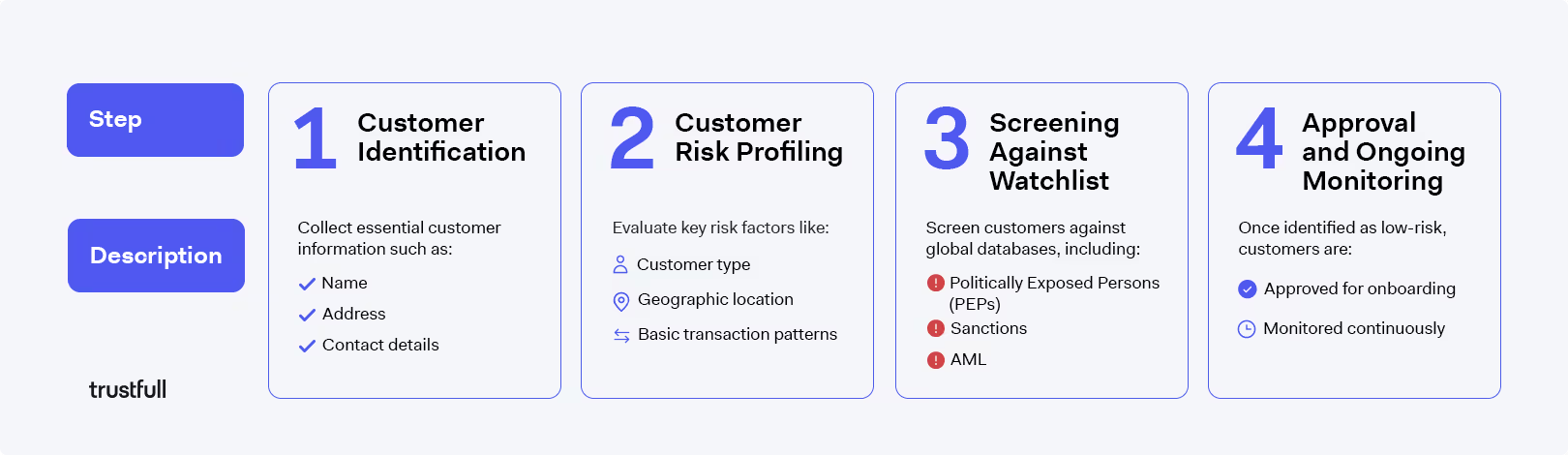

The Simplified Due Diligence (SDD) process involves several key steps designed to verify the identity of low-risk customers efficiently.

Here’s how a typical SDD process is structured:

- Customer identification: the first step in the SDD process is collecting basic customer information, such as name, address, and contact details. This data forms the foundation for initial customer verification.

- Customer risk profiling: financial institutions perform a basic risk assessment by evaluating factors such as customer type, geographic location, type of financial product or service on offer. This step helps categorize the customer as low risk, making them eligible for SDD. When requesting or extracting data to determine a customer's risk, compliance teams can leverage identity intelligence (more on this below) to enhance their assessment with important trust and risk signals.

- Screening against watchlists: customers are screened against international databases, such as politically exposed persons (PEPs) lists or sanctions lists, to ensure they do not pose a higher risk of financial crime.

- Approval and ongoing monitoring: once a customer is identified as low-risk, they are approved for onboarding. After that, ongoing monitoring is required on all customers as an essential way to track any changes in behavior or risk status, ensuring that compliance is maintained throughout the relationship.

Although traditional methods have been effective in assessing eligibility for Simplified Due Diligence, new tech solutions are making it possible to further streamline the process.

Unlock sharper SDD with identity intelligence and risk scoring

As financial institutions face increasing volumes of customers and transactions, traditional methods for determining Simplified Due Diligence (SDD) eligibility can become inefficient. This is where identity intelligence and risk scoring come into play. This refers to the use of digital signals on user attributes such as phone numbers, email addresses, IP addresses, and device fingerprints, to enrich the SDD process, making it more accurate without impacting the customer onboarding experience.

Digital signals enable financial institutions to gather real-time data on customers, validating their identity through multiple third-party sources without requiring additional documentation. For instance, phone numbers can be checked for SIM swapping, email addresses can be cross-referenced with breach databases, and IP addresses can be analyzed for geographical mismatches or suspicious activity. If these signals are used in combination, especially when cross-referencing data from different sources, they give a deeper and more comprehensive view of the customer's legitimacy.

In addition, risk models can be employed to dynamically assign a score based on the data collected. These models analyze hundreds of digital signals as well as patterns of behavior and anomalies, making it easier for businesses to assess risk without manual intervention. This way, a low-risk score can indicate a customer is eligible for SDD, while a higher score might trigger Enhanced Due Diligence.

Risk scoring and identity intelligence streamline SDD processes for financial services, improving efficiency and reducing the risks associated with relying solely on traditional methods.

The benefits of combining SDD with digital signals

As explained, digital signals on users’ phone numbers, emails, and IP addresses can help verify the identity of low-risk customers without requiring excessive documentation, preserving the frictionless customer experience that SDD usually entails.

Moreover, this combined approach reduces the likelihood of errors and human bias that may arise from manual checks, making it possible to detect potential fraud or money laundering activities early. Using real-time data and sophisticated scoring algorithms has many advantages for financial institutions, which can adjust their risk thresholds dynamically and achieve better customer segmentation. This means that low-risk customers can enjoy faster onboarding, while high-risk customers get flagged for further investigation before they pose a threat.

How Trustfull balances efficiency and security in SDD

In short, when digital signals and identity intelligence are integrated into the SDD process, businesses can enjoy the best of both worlds: maintaining operational efficiency while minimizing risks.

At Trustfull, we specialize in providing cutting-edge identity intelligence to help businesses enrich the due diligence process with highly actionable digital signals, reducing the time and cost associated with manual checks. Our platform and API gather and analyze 500+ digital signals on users’ attributes such as email addresses, phone numbers, IP addresses, browsers, and devices. In a matter of seconds, compliance teams can get a 360° view of their customers, spotting red flags such as inconsistencies in their digital footprint at the very beginning of the business relationship.

Additionally, Trustful’s risk scoring capabilities make it easy to detect potential threats, even within low-risk customer segments. This approach helps financial institutions meet their regulatory obligations without sacrificing customer experience, especially in industries where quick onboarding is critical, such as fintech and digital banking.

Another benefit of this combined approach is to protect organizations against certain risks of SDD, such as inadvertently onboarding fraudulent customers. When enriched with digital signals and risk scoring, Simplified Due Diligence balances compliance, efficiency, and security more effectively.

To experience the power of Trustfull’s Identity Intelligence solution in action, sign up for a free trial here or request a demo of our solution here.